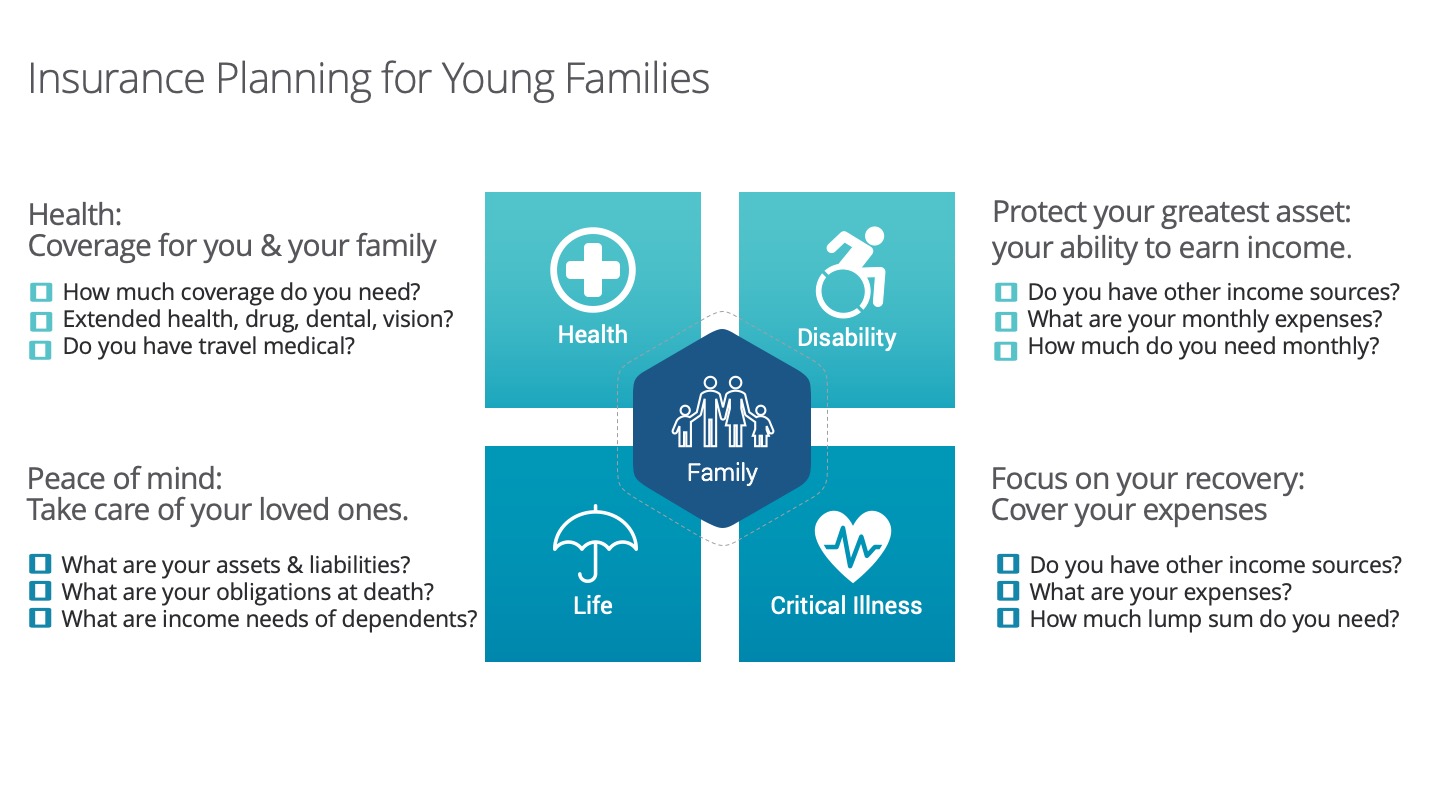

What is Critical Illness Insurance?

Nowadays, people survive serious medical issues such as cancer, a heart attack, or a stroke. And while this is good news if a critical

illness happens to you – your recovery may come with costs that you don’t have the money to cover.

This is where critical illness insurance can play a crucial role. In this article, we’ll explain:

- What critical illness insurance is.

- What you can use the money from a critical illness insurance payout for.

- How you can get critical illness insurance.

What is critical illness insurance?

A critical illness policy is designed to help you pay the costs associated with a serious medical issue such as cancer, a stroke or a

heart attack. With critical illness insurance, your insurance company will issue you a lump-sum payment once the waiting period has passed.

Critical illness insurance can help you pay for costs that aren’t covered by other health plans or disability insurance.

What can I use the money from critical illness insurance for?

With a critical illness lump-sum payment, there are no restrictions on what you can use the money for. You can choose to use the money

to:

- Pay down debt or cover costs such as travel to and from your treatment.

- Cover lost income for you if you cannot work. This is especially important if you are self-employed.

- Pay for a caregiver or lost wages if your spouse takes time off work to be a caregiver.

- Cover renovations on your house that are necessary due to your illness.

- Cover medical treatments and medications not covered by a government or private health plan.

Being able to spend your critical illness insurance lump-sum payment freely takes a lot of stress off you and your family.

How do I get critical illness insurance?

We can help you get critical illness insurance. If you’re interested in critical illness insurance, these are the steps you’ll need to follow:

- Think about why you want critical illness insurance and what kind of coverage you need.

- Book an appointment to speak to us. Apply for coverage.

- We’ll let you know when you’re approved and deliver your policy.

If you do get any of the illnesses listed in your policy, contact us, and we’ll guide you through the steps you need to file a claim. After your claim is approved, we’ll let you know when to expect your lump-sum payment.

Contact us!

It can be scary to think about getting ill, but critical illness insurance can help put your mind at ease that you’ll have the financial

resources you need. Reach out to us today to learn more!