Setting Up Your Employee Benefits Program

In the competitive landscape of today’s business world, an effective employee benefits program stands as a cornerstone of organizational success. Such programs not only serve as magnets for top talent but also highlight an organization’s unwavering commitment to the holistic well-being of its workforce.

Establishing a Benefits Budget

The foundation of a robust benefits program is a well-thought-out budget. By assessing the financial health of your organization, you can determine the funds you’re willing to allocate towards a comprehensive employee benefits package. It’s essential to delve deep into a cost analysis for each potential benefit, ensuring that the budget aligns with both the company’s capabilities and the employees’ needs.

Deciding on the Right Benefits

Once the budget is set, the next step is to curate the benefits that will form part of your program. Choices abound, from group health, dental, and vision insurance to paid time off, retirement savings plans, and flexible health savings accounts. There are also group life and disability insurance options, not to mention perks that foster a healthy work-life balance. While the budget will inevitably influence the selection, it’s paramount to weigh in the preferences and necessities of your employees.

Choosing a Benefits Provider

With a list of desired benefits in hand, the focus shifts to selecting the right provider. This involves researching providers that cater to your chosen benefits and juxtaposing the advantages and costs of each. Given the intricate nature of benefits plans, seeking expert advice can be invaluable in navigating this terrain and ensuring the best fit for your organization.

Finalizing the Benefits Program

After zeroing in on a provider, the next phase is to cement the details of your benefits program. This encompasses signing all requisite documentation and earmarking the date when the plan will kick off. While this might seem like a daunting task, remember that expert guidance can streamline the process, ensuring all i’s are dotted and t’s are crossed.

Communicating the Plan to Employees

The establishment of a benefits program is only half the battle. The other half is effective communication. Organize sessions to walk your employees through the nuances of the benefits plan, addressing any questions or concerns they might harbor. Furnish them with digital or printed copies of the benefits, elucidating both the costs they would incur and the contributions made by the company. It’s pivotal to ensure that every employee has a clear understanding of their benefits, coverages, and the provisions for their dependents. An online portal or resource can further empower employees to delve into their benefits at their own pace. And don’t forget to spotlight your benefits program on your organization’s career page and in job listings.

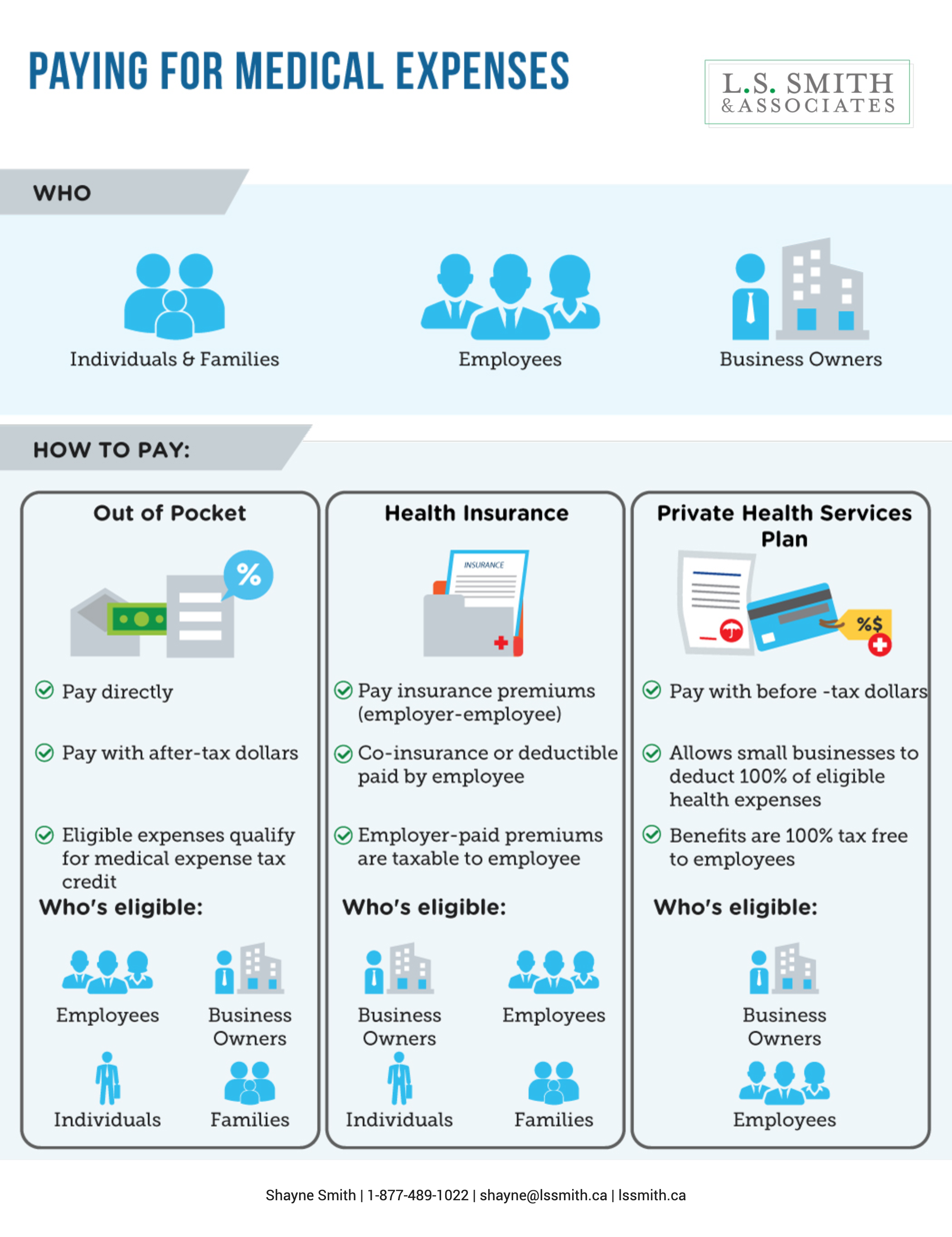

Tax Implications of Group Benefits

A noteworthy aspect of group benefits is their tax implications. Such benefits can be deducted before tax withholdings on an employee’s paycheck. For instance, if group health insurance premiums are covered by the organization, these amounts are eligible for deductions.

In Conclusion

Crafting a comprehensive employee benefits program is more than just a strategic move; it’s an investment in the future of the organization and its people. By adhering to the steps outlined, businesses can sculpt a benefits program that is both versatile and resonant, ensuring a harmonious and productive workplace.