The end of 2024 is quickly approaching – which means it’s time to get your paperwork in order so you’re ready when it comes time to file your taxes!

In this article, we’ve covered five different major types of 2024 personal tax tips:

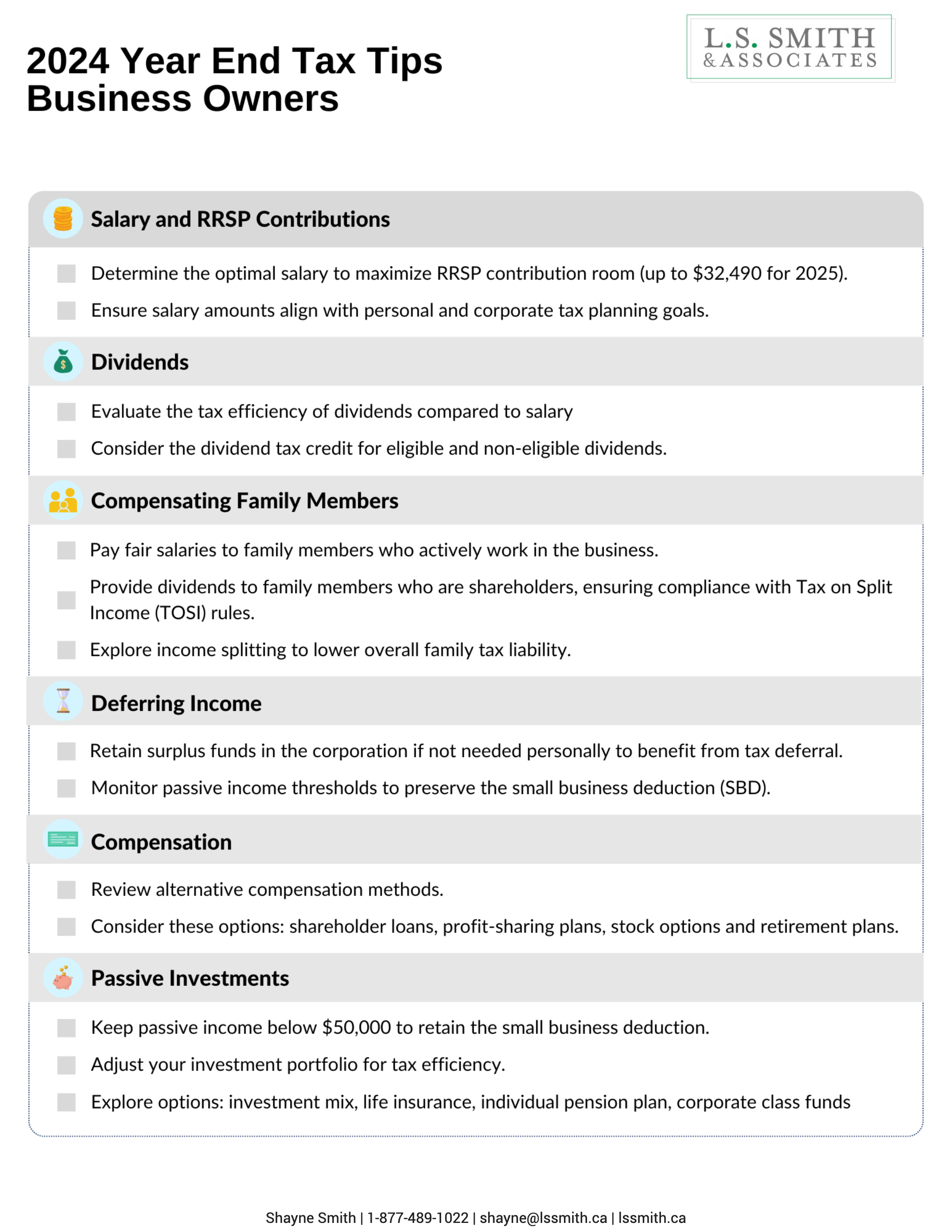

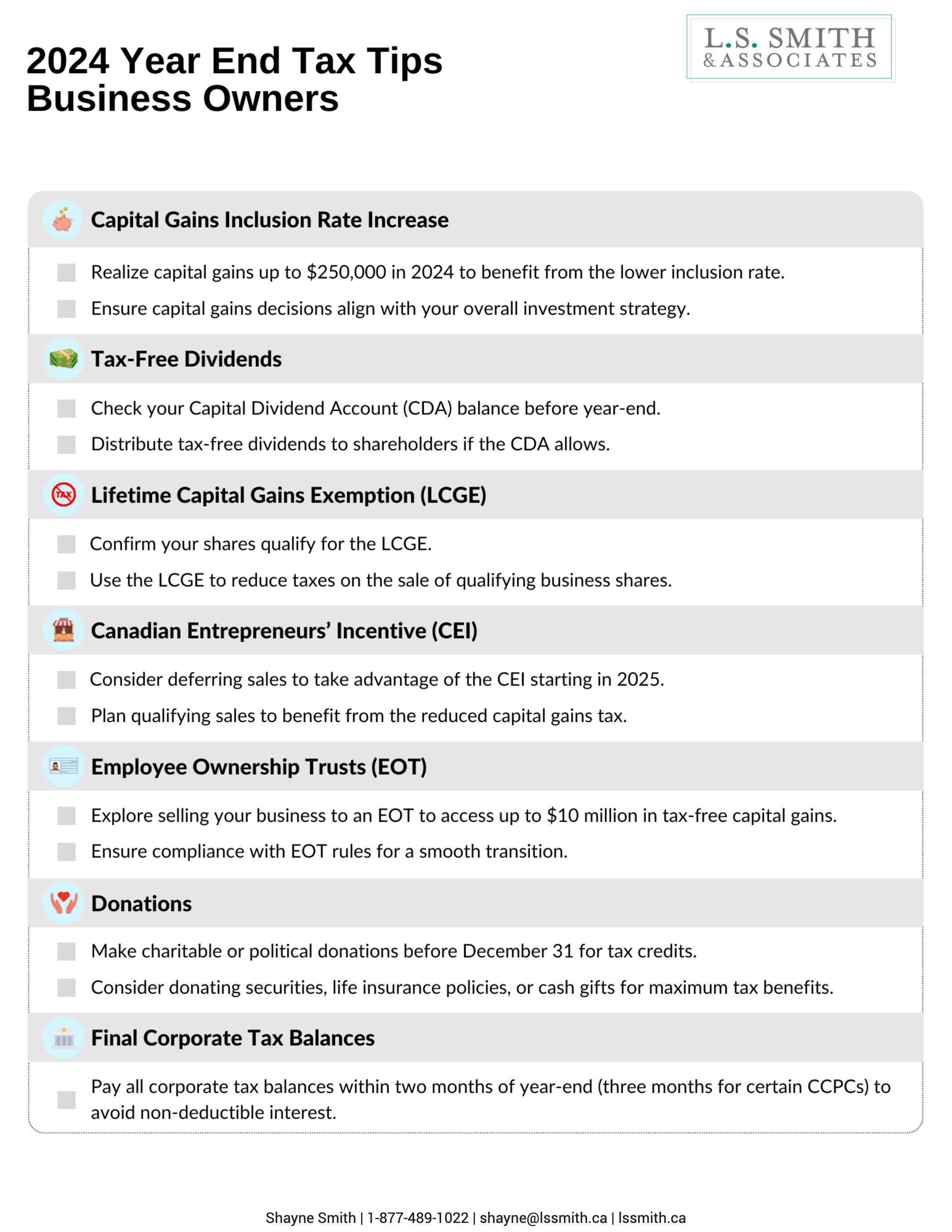

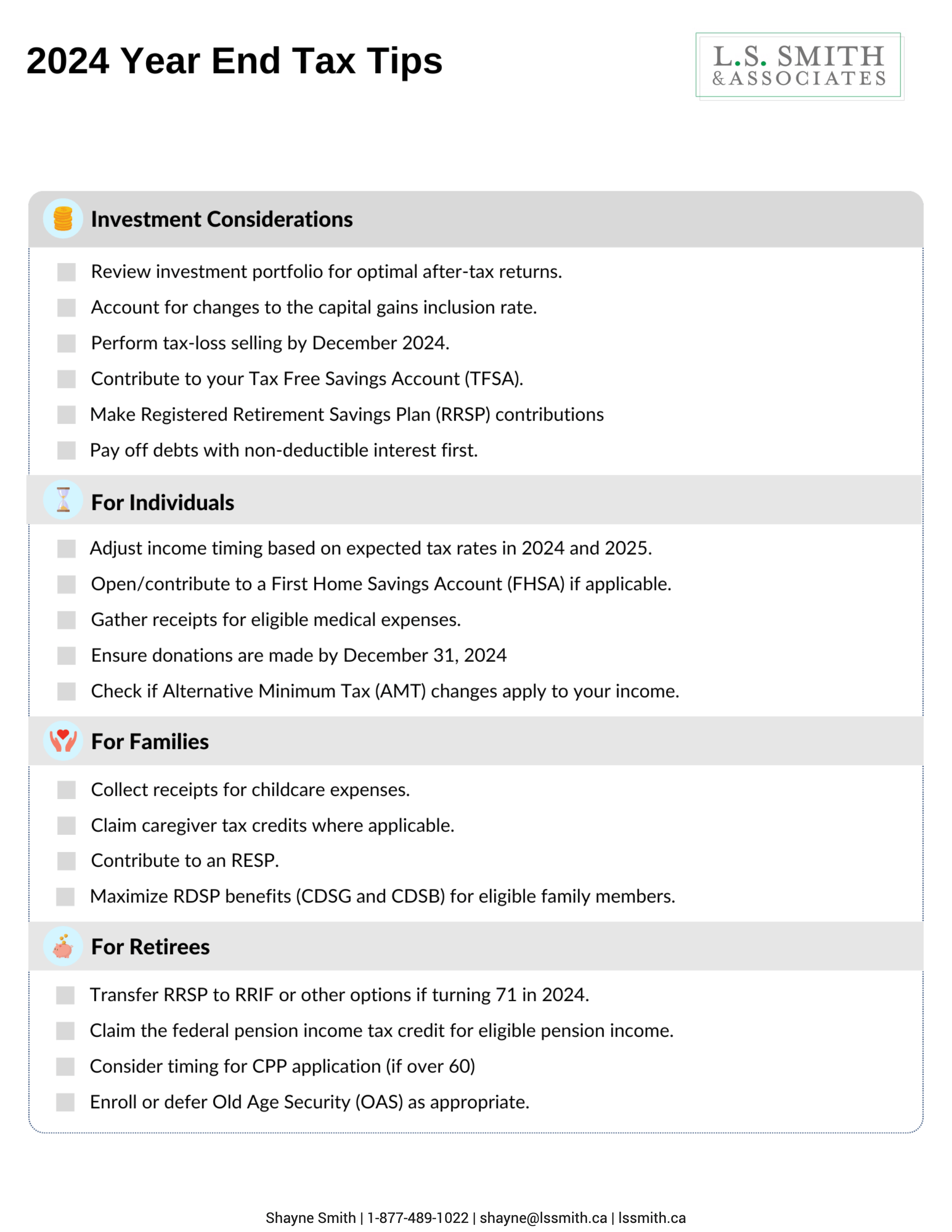

Investment Considerations

Investment Portfolio Mix

Different investments are taxed differently, so reviewing your portfolio ensures optimal after-tax returns. With the recent increase to the capital gains tax rate on gains realized after June 24, 2024, it might make sense to focus on investments that yield eligible dividends instead of capital gains. Whether this works for you depends on your marginal tax rate and where you live, so take some time to evaluate your options.

Capital Gains Inclusion Rate

The 2024 federal budget introduced changes to the capital gains inclusion rate that could affect your tax planning. For individuals, the first $250,000 of annual capital gains remain taxed at the 50% inclusion rate. However, any gains exceeding this threshold are now taxed at 2/3 of the total. If this applies to you, consider strategies like tax-loss selling to offset realized gains.

Tax-Loss Selling

Selling investments in non-registered accounts with losses can offset capital gains elsewhere in your portfolio. Unused net capital losses can be carried back up to three years or forward indefinitely to offset gains in other years. To ensure the loss applies for 2024 (or the prior three years), the transaction must settle within 2024.

Be aware of the “superficial loss” rule: if you or an affiliated person repurchases the same investment within 30 days before or after the sale, the loss cannot be used to reduce taxes immediately. Instead, it’s added to the cost of the repurchased investment, and you’ll benefit from the loss when you sell it later.

Tax-Free Savings Account (TFSA)

You can contribute up to a maximum of $7,000 for 2024. You can carry forward unused contribution room indefinitely. The maximum amount you’re allowed to make in TFSA contributions is $95,000 (including 2024) if you have been at least 18 years old and resident in Canada since 2009.

Registered Retirement Savings Plan (RRSP)

For the 2024 tax year, you have until March 3, 2025, to contribute to your Registered Retirement Savings Plan (RRSP) or a spousal RRSP. However, contributing earlier can benefit you more due to tax-deferred growth. Your deduction limit for 2024 is 18% of your 2023 income, up to $31,560, but this will reduce if you have pension adjustments. Don’t forget, any unused contribution room from previous years or pension adjustment reversals can increase your limit.

Also, you can deduct contributions on your 2024 income if they are made within the first 60 days of 2025. It’s possible to defer these deductions to a later year if that suits your financial strategy better.

Interest Deductibility

If you can, focus on paying off debts with non-deductible interest first, like personal loans or those with non-refundable credits (e.g., student loans). Use borrowing for investment or business purposes and save your cash for personal expenses.

For Individuals

Income Timing

If your marginal personal tax rate is lower in 2025 than in 2024, defer the receipt of certain employment income; if your marginal personal tax rate is higher in 2025 than in 2024, accelerate.

First Home Savings Account (FHSA)

If you are a Canadian resident, age 18 or older and planning to become first-time homebuyers. Starting from April 1, 2023, this account serves as a valuable tool for saving towards the purchase of a qualifying first home.

The FHSA program comes with an annual contribution limit of $8,000, and a cumulative lifetime cap of $40,000, with the flexibility to carry forward up to $8,000 in unused contributions. Importantly, contributions made to the FHSA are tax-deductible, offering potential tax benefits. Additionally, the returns earned on your savings within this account are not subject to taxation, which can enhance the overall growth of your savings. Most notably, when you make qualifying withdrawals to buy your first home, these withdrawals are non-taxable.

Medical expenses

If you have eligible medical expenses that weren’t paid for by either a provincial or private plan, you can claim them on your tax return. You can even deduct premiums you pay for private coverage. Either spouse can claim qualified medical expenses for themselves and their dependent children in a 12-month period, but it’s generally better for the spouse with the lower income to do so.

Charitable Donations

Federal and provincial donation tax credits can significantly reduce your taxes, with the savings depending on your province. Larger donations receive higher federal credits, and you can pool receipts with your spouse or carry them forward for up to five years.

For 2024, changes to the Alternative Minimum Tax (AMT) limit the portion of the donation credit that can be applied for AMT purposes. Be sure to make your donations by December 31 to claim them for 2024.

Alternative Minimum Tax (AMT)

The Alternative Minimum Tax (AMT) ensures a minimum level of tax is paid by limiting certain deductions, exemptions, and credits. If your AMT calculation exceeds your regular tax, you’ll pay the difference as AMT for the year.

Revised for 2024, AMT changes include a higher tax rate, a larger exemption, and stricter limits on tax-reducing measures like capital gains, stock options, Canadian dividends, and non-refundable tax credits. These changes may increase your AMT if your taxable income exceeds $173,205.

For Families

Childcare Expenses

If you paid someone to take care of your child so you or your spouse could attend school or work, then you can deduct those expenses. A variety of childcare options qualify for this deduction, including boarding school, camp, daycare, and even paying a relative over 18 for babysitting. Be sure to get all your receipts and have the spouse with the lower net income claim the childcare expenses. In addition, some provinces offer additional childcare tax credits on top of the federal ones.

Caregiver

If you are a caregiver, claim the available federal and provincial/territorial tax credits.

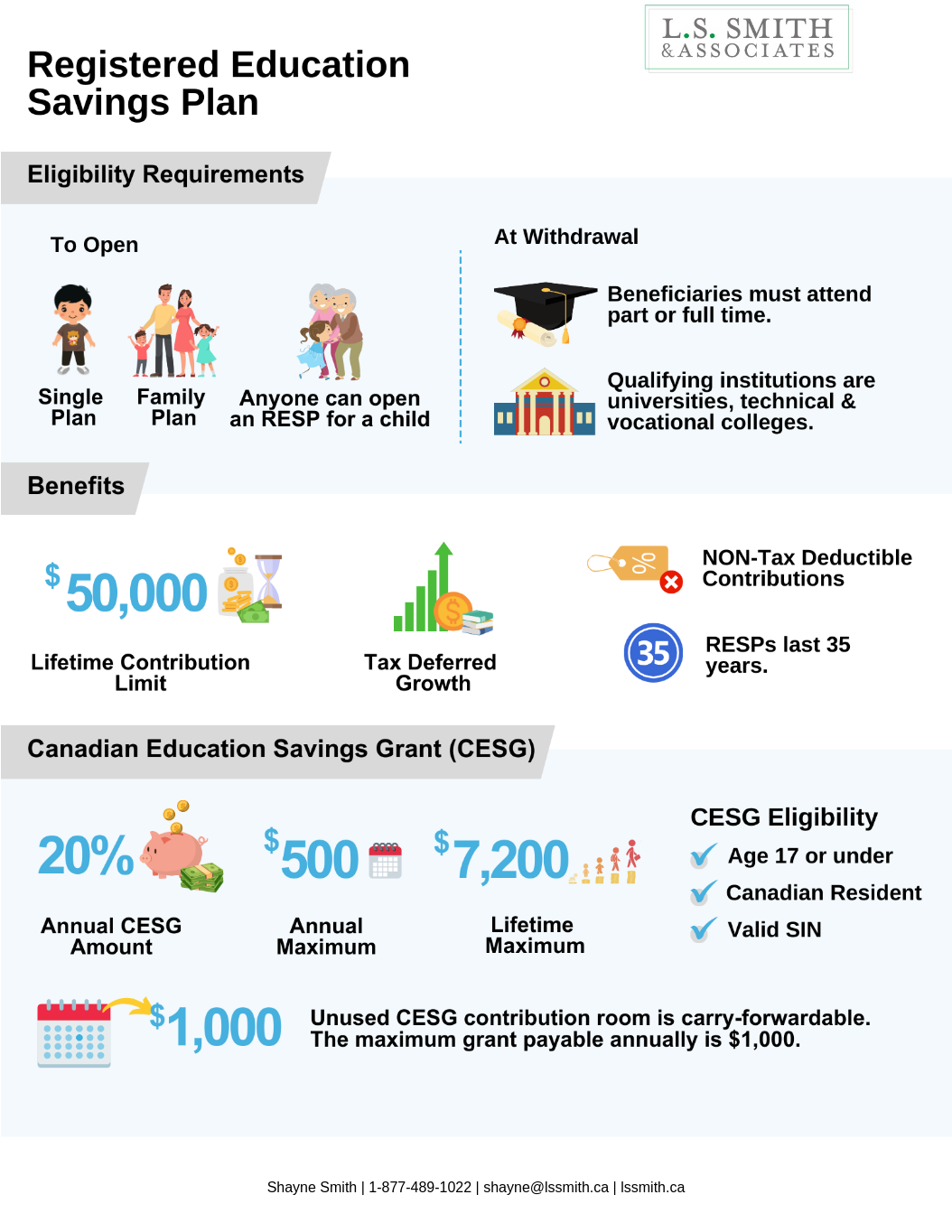

Registered Education Savings Plan (RESP)

RESP can be a great way to save for a child’s future education. The Canadian Education Savings Grant (CESG) is only available on the first $2,500 of contributions you make each year per child (to a maximum of $500, with a lifetime maximum of $7,200.) If you have any unused CESG amounts for the current year, you can carry them forward. If the recipient of the RESP is now 16 or 17, they can only receive the CESG if a) at least $2,000 has already been contributed to the RESP and b) a minimum contribution of $100 was made to the RESP in any of the four previous years.

Registered Disability Savings Plan (RDSP)

If you have an RDSP open for yourself or an eligible family member, you may be able to get both the Canada Disability Savings Grant (CDSG) and the Canada Disability Savings Bond (CDSB) paid into the RDSP. The CDSB is based on the beneficiary’s adjusted family net income and does not require any contributions to be made. The CDSG is based on both the beneficiary’s family net income and contribution amounts. In addition, up to 10 years of unused grants and bond entitlements can be carried forward.

For Retirees

Registered Retirement Income Fund (RRIF)

Turning 71 this year? If so, you are required to end your RRSP by December 31. You have several choices on what to do with your RRSP, including transferring your RRSP to a registered retirement income fund (RRIF), cashing out your RSSP, or purchasing an annuity. Talk to us about the tax implications of each of these choices.

Pension Income

Are you 65 or older and receiving pension income? If your pension income is eligible, you can deduct a federal tax credit equal to 15% on the first $2,000 of pension income received – plus any provincial tax credits. Don’t currently have any pension income? You may want to think about withdrawing $2,000 from an RRIF each year or using RRSP funds to purchase an annuity that pays at least $2,000 per year.

Canada Pension Plan (CPP)

If you’ve reached the age of 60, you may be considering applying for CPP. Keep in mind that if you do this, the monthly amount you’ll receive will be smaller. Also, you don’t have to have retired to be able to apply for CPP. Talk to us; we can help you figure out what makes the most sense.

Old Age Security (OAS)

If you’re 65 or older, enrolling in OAS is essential. If your income exceeds OAS thresholds, strategies like income splitting can help reduce clawbacks.

You can defer OAS for up to 60 months, increasing your monthly payment by 0.6% for each month deferred. Planning ensures you maximize your benefits and optimize your retirement income.

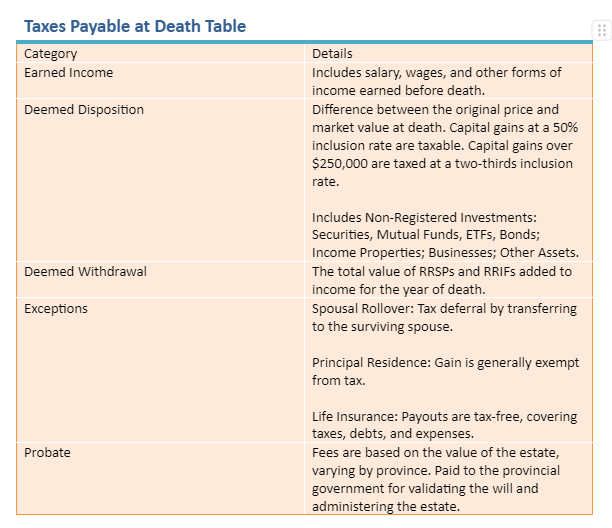

Estate planning arrangements

Regularly reviewing your estate plan is essential to ensure it aligns with your objectives and complies with current tax laws. An annual review allows you to adjust for life changes and legal updates, keeping your plan effective. Additionally, exploring strategies to minimize probate fees can preserve more of your estate for your beneficiaries. Regularly examining your will ensures it remains valid and reflects your current wishes.

For Students

Education, tuition, and textbook tax credits

If you’re attending post-secondary school, claim these credits where available.

Canada tuition credit

If you’re between 25 and 65 and enrolled in an eligible educational institution, you may be eligible for the Canada Training Credit, a refundable tax credit designed to help cover tuition and other fees associated with training. Additionally, you can claim tuition paid on your taxes, carry forward unused amounts to future years, or transfer unused tuition amounts to a spouse, parent, or grandparent.

Need some additional guidance? Reach out to us if you have any questions. We’re here to help.

-Shayne-Smith-N2cCT9YpXqWbeLbXq.png)

-Shayne-Smith-N2cCT9YpXqWbeLbXq.png)

-Shayne-Smith-N2cCT9YpXqWbeLbXq.png)

-Shayne-Smith-N2cCT9YpXqWbeLbXq.png)